Is your agency still spending most of its marketing budget chasing brand-new customers?

That is the most expensive way to grow your bottom line.

In fact, the best insurance carriers and agencies use a better model. Instead of fighting for new logos, they mine the customers already on their books.

This guide shows you how AI chatbots help cross-sell insurance policies on their own. And in doing so, shows how doing this helps insurance firms add to thier revenue!

What Is Cross-Selling in Insurance?

Cross-selling is a process where the salesperson or insurance agent identifies an existing policyholder who owns one insurance policy and tries to sell them another.

Why? Well, A client insures their car to meet state law.

However, that same client may also be buying a house! They may be starting a family or may even be planning for retirement…

A current customer buys a second policy 60% to 70% of the time.

Bundling helps the customer too by adding multi-line discounts. And in doing so, it brings one bill and one claims process. A new policyholder costs 7 to 9 times more than an existing one. Most agencies still spend as if new business is the only lever.

For the carrier, bundling means a higher premium per customer. It also means lower cost per sale. But best of all, it means a customer who is hard for a rival to steal.

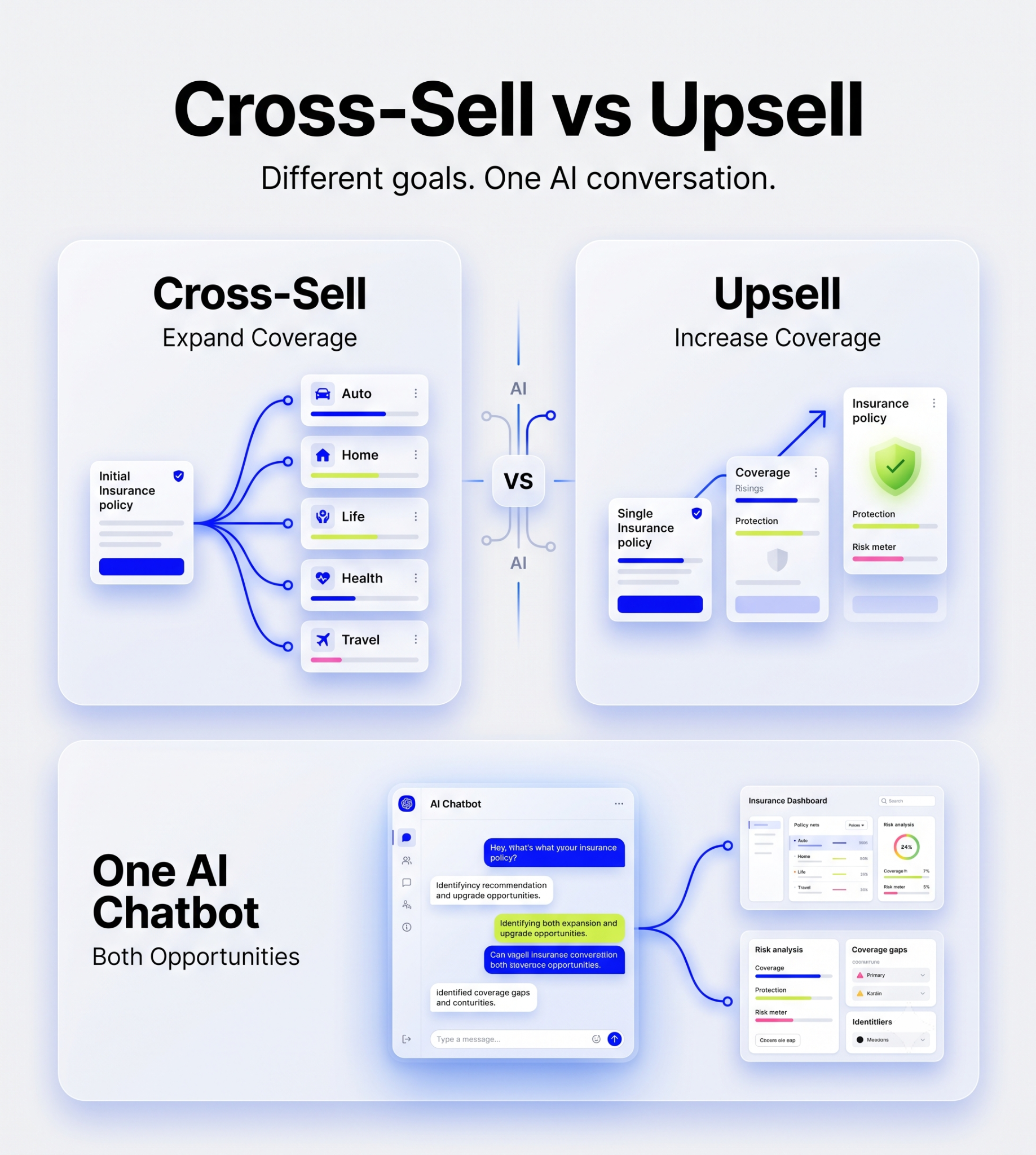

Cross-Selling vs Upselling

Cross-selling vs upselling insurance plans are - two terms get used interchangeably, but they solve different problems!

Upselling deepens a risk category the customer already owns, like raising a liability limit. Cross-selling expands the relationship into a category the customer does not yet own.

AI chatbots help cross-sell insurance both ways in the same conversation. The better AI chatbots for insurance agencies can flag that a current deductible is too high while quietly checking whether the household has any uninsured exposure at all.

Why Traditional Insurance Cross-Selling Often Falls Short

The financial case for how chatbots help cross-sell insurance is clear! Execution is where it breaks down.

- Limited Agent Availability: Producers handle claims. They handle paperwork. They chase big accounts. A $15-a-month renter's policy does not earn their time. So it never gets pitched.

- Generic Product Recommendations: Policy data often sits stuck in an old system. It is cut off from marketing tools. A ten-year client with three policies gets the same bundle email as a new customer.

- Missed Opportunities During Customer Interactions: A new baby. A first home. A big purchase. These moments create new coverage needs. Most of that research happens online. No signal reaches a human agent.

- Inconsistent Follow-Ups: A customer shows interest in an umbrella policy. They want to check with their spouse first. No one follows up, and his interest fades - meaning, the policy never gets written!

How Chatbots Help Cross-Sell Insurance Products - 6 Ways

A conversational AI chatbot for insurance does not get tired, prioritize big commissions, or forget a follow-up. AI tools for insurance agents like chatbots works through six distinct, automated pathways to surface and close cross-sell opportunities.

1. Analyzing Customer Data and Policy History

For instance, if an auto customer messages in to download an ID card and the bot notices their vehicle is seven years old with no roadside assistance, it can automatically turn a routine request into a revenue moment.

A human insurance agent would have to open several AMS screens JUST to spot that gap.

But, before a chatbot replies to a single message, it evaluates the full customer record:

- Existing policies: Every active line of coverage, including deductibles and limits.

- Coverage gap: An area where the client is uninsured due to an unknown risk.

- Client demographics: Age, geography, and income are used to anticipate future needs.

- Renewal dates: The exact date at which an existing policy must be reviewed.

2. Recommending Products During Conversations

The most reliable AI chatbots in insurance help cross-sell insurance when they read intent, not just respond to it. Timing is the whole advantage, the offer arrives while the customer is already engaged.

In this case, the recommendation is added within an existing plan from the customer, making it seem helpful rather than marketing-oriented.

Done correctly, this can increase cross-selling profits between 15% and 25%. This works for any standard service interaction:

- Quote requests: Show the marginal cost of comprehensive coverage next to a state-minimum quote.

- Claims inquiries: Introduce accident forgiveness while the cost of risk is still top of mind. Not to mention AI tools for claims processing that can reduce repetitive tasks or hard parts that eat into agents’ time.

- Billing questions: Suggest bundling a monoline policy to unlock a multi-line discount.

- Policy servicing: Recommend a property rider when a customer updates their address.

3. Identifying Coverage Gaps Automatically

No human auditing cycle is fast enough to catch this volume of detail across an entire book.

The chatbot does not wait for a conversation to find a gap, it audits the book continuously by doing this like:

- A homeowner with no flood insurance gets flagged the moment updated flood-zone data shows new exposure.

- A breadwinner with a $1 million life policy but zero disability coverage gets surfaced automatically, before an agent ever notices.

4. Delivering Personalized Product Suggestions

Static, single-trigger campaigns are easy to ignore. This is why, for insurance companies, layering these signals for chatbots help cross-sell insurance with a relevant offer that is a lot more personalized than a mass email.

At this depth, personalization has been linked to revenue lifts of 10% to 30%.

The recommendation that reaches the customer with these signals reflects their actual life, not a generic segment. A chatbot builds its recommendation from several signals at once:

- Behavioral signals: Pages browsed before opening the chat window.

- Past purchases: Risk tolerance and premium appetite over time.

- Family status: A marriage, birth, or divorce that shifts coverage priorities.

- Vehicle and property ownership: A new car or new home that opens an obvious need.

5. Cross-Selling During Renewals

Renewal is the ultimate time to talk about cross-sells.

It’s the only period when the customer is evaluating coverage and price.

How do chatbots help cross-sell insurance here? Well, The bot considers tenure, as well. It talks to one-year clients differently than ten-year veterans.

An auto-renewal chatbot can suggest:

- Roadside Assistance: Presented as an insignificant add to an already established policy.

- Coverage for Rental Car Reimbursement: Supported by the customer’s past claims record.

- Home Insurance Policy Package: Sold with a computed multi-line discount in real-time.

6. Automating Follow-Ups and Lead Nurturing

Complex policies rarely close in one conversation, they need time, and comparison!

But also, often, a word with thier spouse.

The sequence keeps working for days or weeks until the lead converts or opts out.

In case the customer is interested but does not conclude the conversation, the chatbot can become useful through continuous interaction with the prospect rather than leaving it idle:

- SMS: Brief message with the button leading to the current offer.

- WhatsApp: A brochure or comparison chart on the exact coverage discussed.

- Email: A summary of the unmet need, with a direct link to the resume.

- Website chat: The conversation picks up exactly where the customer left it.

Top Insurance Cross-Selling Use Cases for Chatbots

- Auto Insurance to Home Insurance: The most common and most profitable bundle, surfaced the moment a customer touches their auto policy.

- Health Insurance to Critical Illness Coverage: Positioned as cash for living expenses, alongside a primary plan that only covers hospital bills.

- Life Insurance to Disability Insurance: Closes the far more statistically likely gap that a term policy leaves open.

- Home Insurance to Flood Insurance: Tracked using geolocation technology when a property is within an altered flood zone area.

- Travel Insurance Extra Coverage: Access to lounges, limits on medical evacuation, and equipment coverage according to your destination.

- Small Business Insurance Package: Including cyber liability and business interruption coverage together with the basic general liability insurance.

How Thunai AI-Powered Chatbots Improve Insurance Cross-Selling

Basic, rule-based bots can deflect FAQs along a rigid decision tree.

Basic chatbots cannot help cross-sell insurance since they cannot read context, resolve conflicting policy data, or hold a compliant, nuanced product conversation.

Thunai AI for insurance is built for the harder problem.

Basically, Thunai Brain brings policies, claims information, and consumer history into a single knowledge graph. And in doing so, it has connectivity with over 50 enterprise systems, such as Salesforce, Applied Epic, and AMS360.

That foundation is what lets Thunai AI chatbots help cross-sell insurance with precision instead of guesswork:

- Predictive Product Recommendations: Thunai watches policy states all the time. It spots a cyber liability or umbrella chance before any agent opens the file.

- Intent Detection: The system reads the real need behind a complaint. It does not just scan for keywords. It then points toward the right coverage gap.

- Customer Segmentation: Revenue AI scores buying signals in every chat. It aims pitches only at strong leads.

- Conversational Personalization: Past chats and claims history shape each reply. The pitch reads like advice, not a script.

- Real-Time Decisioning: Live data lets Thunai decide what to offer right away. It routes hard cross-sells to a human broker, with full context attached.

Want to know how Thunai can help your team? Book a free demo!

Frequently Asked Questions

Can chatbots sell insurance products?

Yes. Modern AI chatbots for insurance can guide a risk check. They can build a bindable quote. They can take payment. They can issue documents on their own. For complex policies, they qualify the lead first. Then they hand it to a licensed agent to close.

How does an insurance chatbot detect a cross-sell opportunity?

AI insurance chatbots analyze the following criteria: demographics, browsing activity, claims history, and policy design. It highlights the obvious gaps. For example, an auto insurance client without renter’s insurance. It is flagged at the appropriate stage of the conversation.

Which insurance products are suitable for cross-selling through chatbots?

The simple AI chatbots for insurance are preferred. Roadside assistance. Rent reimbursement. Renter’s insurance. Liability umbrella. Critical illness. Travel protection. The complex ones are initiated through the bot but then closed by the human adviser.

Are chatbot recommendations compliant with insurance regulations?

Yes, on platforms built for it. Thunai works inside strict rules. It uses human checks. It holds certifications like ISO 42001, SOC 2 Type II, and GDPR. This keeps every offer accurate and safe to defend.

How do chatbots personalize insurance recommendations?

AI chatbots for insurance ombine behavior, purchase history, family status, and asset ownership into one profile. Then they use natural language tools to write a pitch. It reads like real advice, not a mass ad.